When an insured person passes away, a life insurance policy will pay out a lump amount to assist the insured’s dependents and heirs.

As long as the policyholder continues to make insurance premium (payment) installments on the policy, the death benefit coverage is still in place.

The cost of a policy’s premiums will vary depending on the insured’s age, health, and other factors.

The younger and healthier the insured, the less costly the premiums will be. The IRS handles life insurance differently from other kinds of financial products because it is meant to sustain a beneficiary.

When getting life insurance, it’s important to take tax effects into account. Different tax regulations are imposed on various plans by the Internal Revenue Service (IRS), and the differences made are sometimes arbitrary.

The information in the advice that follows is intended to assist clarify some of the tax ramifications related to life insurance premiums.

Table of Contents

Is a Life Insurance Policy’s Cash Value Tax Deductible?

You may often obtain the funds from a cash-value life insurance policy by a withdrawal, a loan, or by surrendering the policy and terminating it.

Having access to the money that accumulates within the policy is one of the benefits of purchasing cash-value life insurance.

Three things typically get your premium payments: cash value, the cost of your insurance, and policy fees and penalties. These can be large amounts, especially if you have loans in parallel.

You shouldn’t skip life insurance payments because it matters. You may want to consider consulting with the best debt consolidation companies bbb to make your payments less painful.

Based on the interest or investment profits it generates, money in the cash value account increases tax-free (depending on the policy). You could have to pay taxes once you withdraw the money, however.

Different tax laws apply if your life insurance policy is a “modified endowment contract,” or MEC, and it’s essential to contact a financial expert to understand the ramifications.

Premiums for Life Insurance are Not Tax Deductible

The IRS often views premium payments as a personal cost similar to rent or food. Thus, you cannot claim premiums as a tax deduction.

Benefits from Death and Other Payments

Beneficiaries often don’t pay taxes on payments from life insurance since the money they get after the insured passes away isn’t regarded as taxable income.

Beneficiaries don’t often need to disclose it to the IRS. But certain insurance benefits could be subject to taxation. A deeper look follows:

Payouts in One Lump Sum: Not Taxable

The face value, or death benefit, of a life insurance policy, is a crucial element. Beneficiaries get this sum upon the insured person’s death.

The money is not taxed if the recipient elects to receive it all at once.

Taxable Interest on Installment Payments

The insurer places the whole death benefit into an interest-bearing account if a recipient opts to receive payments in installments rather than a lump amount.

Regular payments reflecting the principle (the policy’s face value) plus interest are sent to the recipient. While the interest earned is taxed as ordinary income, the principle component is not.

Three Distinct Parties are Involved in the Policy

If separate persons carry out each of the three functions specified in the insurance, the death benefit can be liable to gift tax:

- The insured: a person whose life is covered by the insurance.

- The policy owner: the individual who purchases and/or is the policy’s owner.

- The beneficiary: the individual who will be compensated if the insured party passes away.

There are often just two parties involved. For instance, if you purchase insurance for yourself, your kid will be the beneficiary of the death benefit.

However, the IRS views the death benefit as a gift from the policy owner to the beneficiary if a separate individual performs each function.

The death benefit, for instance, is legally a gift from you (the owner) to your kid if you purchase a policy to cover your spouse’s life with your child as the beneficiary (the beneficiary).

You may be subject to gift tax if you are the insurance owner and are regarded as the giver.

Your loved ones probably won’t have to pay gift tax because of how it is structured. When you pass away, the tax won’t become payable until your estate, including any gifts you made worth more than $16,000 per year per recipient, is valued at more than $12.06 million.

The general rule is that you must file a gift tax return even if you don’t wind up paying gift tax on any sizeable contributions (IRS Form 709).

Are Profits From Life Insurance Taxable?

Dividends are normally exempt from taxation since the IRS views them as premium refunds. The profits you get, however, are taxable if the insurer holds the payouts in an interest-bearing account.

The difference is normally taxed if you get more in dividends than you have previously paid in premiums.

Life Insurance Supplied By Your Employer Can Be Taxed

You can owe income tax on a portion of the value of the life insurance provided to you by your employer as a benefit.

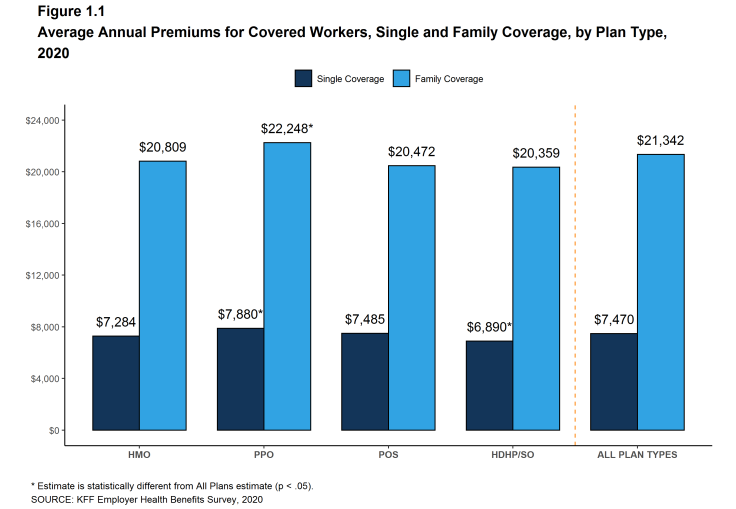

Average annual insurance premiums for insured workers for families are higher than for single people. Family insurances go over $20,000, which will be tax-free.

Workplace insurance with a death benefit of up to $50,000 is tax-free; but, for any amount beyond that, the premiums your company pays are considered part of your taxable income. (The increased premiums are not taxed if you pay them yourself.)

Additionally, if your company’s policy has a cash value component, whatever interest you receive on it is taxable income.

You won’t have to pay taxes on those gains until you cash in the insurance policy, however.

Conclusion

Sales tax is often not applied to life insurance premiums, and they are typically not tax-deductible either.

However, there are several situations in which the IRS may interpret life insurance premiums differently and you will suffer from particular tax repercussions. These situations usually occur when a company purchases or owns a life insurance policy.

Originally posted 2022-11-11 11:37:52.

Hello, I am a professional writer and blogger at Adclays.com. I love to explore the latest topics and write on those topics. I spend the maximum of my time on reading and writing interesting topics which provide valuable piece of information to my readers whether it comes to the latest fashion, technology, healthy lifestyle, business information, etc. Explore my writings by visiting the website.